The Corporate Sustainability Reporting Directive (CSRD) represents a transformative step in sustainability reporting within the European Union. It introduces rigorous requirements that expand the scope of sustainability reporting, ensuring greater transparency and accountability among businesses. By mandating adherence to the European Sustainability Reporting Standards (ESRS), the CSRD sets a benchmark for environmental, social, and governance (ESG) reporting, integrating it with corporate strategy and performance.

Following on from our recent 5-minute guide that summarised the EU Green Deal and its key directives, our topical article below delves further into the CSRD, the first of three key directives underpinning the EU Green Deal that are most relevant to MedTech companies.

Read on as our Founder Jörg Dogwiler and Head of Regulatory Bruno Gretler walk through the directive’s objectives, requirements, and challenges, as well as some strategic recommendations for Swiss medical device manufacturers.

What does the CSRD replace?

Let’s start with some regulatory context. The CSRD supersedes the Non-Financial Reporting Directive (NFRD), broadening its application from approximately 11,700 companies to nearly 50,000 entities, including non-EU firms with substantial operations within the EU.

These include entities with subsidiaries or listings on EU-regulated markets or those generating over €150 million in EU revenue. This expansion addresses growing stakeholder demands for consistent, reliable, and comparable ESG data, enabling more informed decision-making.

Does the CSRD integrate with broader regulatory frameworks?

The CSRD complements existing EU regulations, including the EU MDR and EU IVDR by emphasising sustainability aspects alongside quality and safety. Additionally, its alignment with the EU Taxonomy for sustainable finance enhances its role in advancing the European Green Deal and Sustainable Finance Package. This integration underscores the interconnectedness of ESG issues and corporate performance, promoting a comprehensive approach to sustainability.

What are the European Sustainability Reporting Standards (ESRS)?

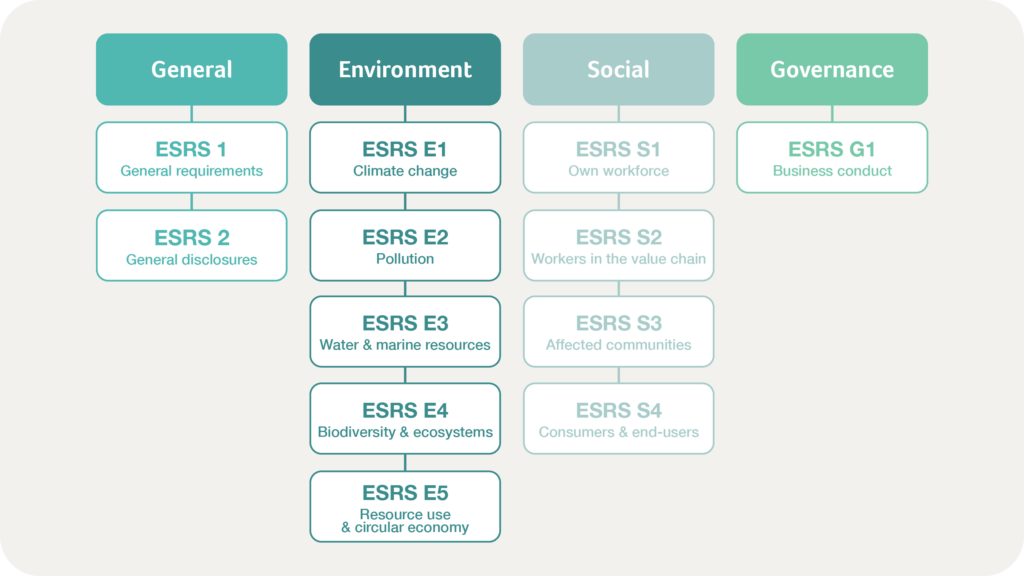

At the core of the CSRD are the European Sustainability Reporting Standards (ESRS). These standards provide a structured approach to sustainability reporting, and are organised under four main categories:

ESRS 1 and ESRS 2 form the foundation of the reporting framework, guiding companies in structuring their reports and identifying material topics. This approach ensures that reports are coherent, focused, and aligned with both regulatory and stakeholder expectations.

What do the four reporting categories under ESRS encompass?

Each of the four ESRS reporting categories serve as a cornerstone for structured and comprehensive sustainability reporting. These pillars encompass various data categories: narrative, quantitative, and monetary – ensuring a balanced and detailed portrayal of a company’s sustainability practices.

General Information

The general information outlined in ESRS 1 and ESRS 2 is mandatory for all companies, regardless of their industry. ESRS 1 establishes the structural foundation for sustainability reports, addressing essential questions such as the organisation’s reporting boundaries, governance structures, and key ESG metrics. ESRS 2 expands on these principles by specifying how companies identify material topics, ensuring alignment with their overall strategy.

Environmental Information

The environmental category focuses on climate change, biodiversity, resource usage, and pollution. Companies must provide detailed data on their CO₂ emissions, energy consumption, water usage, and waste management practices. Reporting on these areas requires companies to evaluate their impact on natural resources and ecosystems comprehensively.

Social Information

This section covers workforce conditions, community impacts, and human rights considerations. Companies are expected to report on diversity, inclusion, labour practices, and their supply chain’s adherence to human rights standards. Transparency in these areas demonstrates a company’s commitment to ethical practices and social equity.

Governance Information

Governance reporting addresses corporate ethics, anti-corruption measures, and board accountability. Companies must disclose their governance structures and policies, ensuring stakeholders understand the mechanisms in place to uphold ethical standards and decision-making processes.

How do I focus my reporting scope?

The ESRS framework encompasses over 1,000 potential disclosure requirements to enable nuanced and sector-specific reporting, but due to the double materiality principle, reporting on every data point is not obligatory.

The double materiality principle ensures a holistic view of a company’s sustainability performance by requiring businesses to assess how sustainability matters impact their operations and how their activities affect environmental and social factors. It also ensures that only relevant topics and associated data points are reported.

For example, if water usage is identified as material, related disclosures such as water consumption and wastewater management become mandatory. Conversely, non-material data points can be excluded, keeping reports concise and focused on significant impacts.

Materiality assessments play a critical role in determining the scope of reporting. Companies must evaluate the relevance of specific ESG factors to their operations and stakeholders, ensuring that reports remain meaningful and avoid unnecessary complexity.

It’s worth noting that medical device companies should be prepared for the external auditing of their sustainability reports, a key aspect of the CSRD which aims to enhance the credibility and reliability of disclosures. Under the directive, companies are also required to integrate sustainability reporting with financial reporting, reflecting the growing importance of ESG factors in corporate strategy.

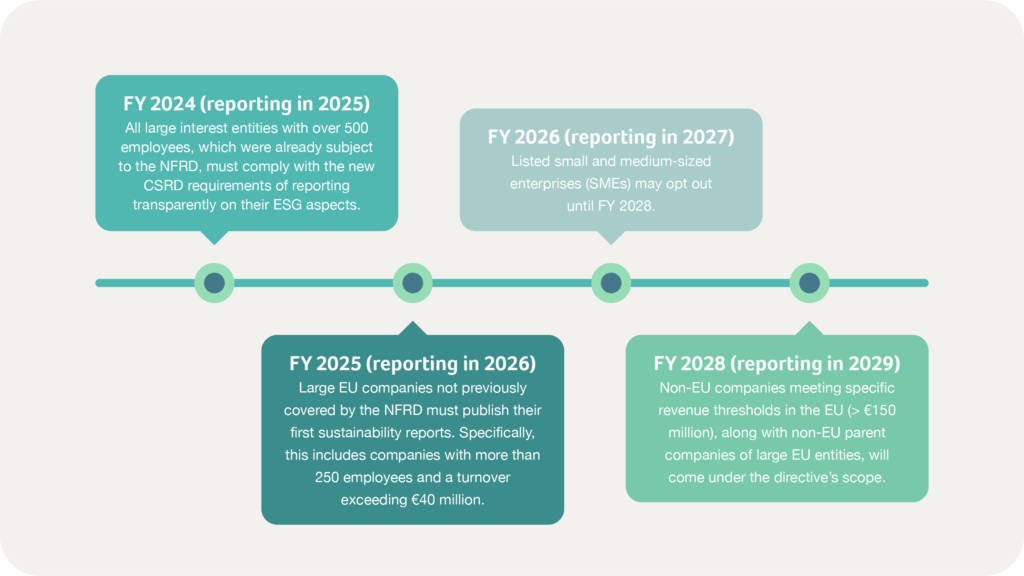

What’s the compliance timeline?

The CSRD’s phased implementation provides companies with time to adapt:

What challenges does CSRD present?

The CSRD’s implementation brings significant challenges. Medical device companies must integrate sustainability reporting into their broader management systems, requiring a shift in organisational culture and priorities. The complexity of supply chains in the medical device industry adds to the difficulty. For instance, ensuring compliance across multi-tiered suppliers in regions with less stringent regulations necessitates robust risk assessments and enhanced transparency.

Swiss medical device manufacturers face unique challenges as non-EU entities. While not directly subject to EU regulations, Swiss companies exporting to the EU must comply with CSRD requirements to retain market access. This poses operational and financial burdens, including the need to establish dedicated teams, and invest in ESG systems, training, and compliance measures.

Despite these challenges, the CSRD offers substantial opportunities. The directive positions sustainability as a competitive differentiator, enabling companies to build stronger reputations and attract ESG-focused investors. By adopting the CSRD framework, organisations can align with global sustainability expectations, secure market access, and innovate through the development of eco-friendly products and circular economy practices.

The ESRS framework further promotes innovation by encouraging companies to rethink supply chains and adopt sustainable materials. For the medical devices industry, this could lead to advancements in product lifecycle management and the implementation of recycling strategies, aligning operational goals with broader ESG objectives.

What action should Swiss medical device manufacturers take?

Facing more thorough reporting obligations, Swiss medical device manufacturers should prioritise comprehensive risk assessments to map supply chain vulnerabilities. Leveraging digital tools such as blockchain for supply chain traceability can improve transparency and accountability. And engaging suppliers through training and long-term partnerships will bolster alignment with sustainability goals and compliance requirements.

More broadly, collaboration between companies within the MedTech industry encourages reduced compliance costs and standardised reporting practices. By participating in industry alliances and forums for example, Swiss companies can share best practices and influence EU discussions on sustainability regulations.

Advocacy and proactive engagement with policymakers can further ensure that sector-specific challenges are adequately addressed.

In summary…

The Corporate Sustainability Reporting Directive marks a pivotal advancement in corporate accountability and transparency. While the CSRD imposes significant obligations, it also provides a framework for innovation, operational improvement, and reputational enhancement.

For Swiss medical device manufacturers and global companies alike, compliance with the directive represents an opportunity to contribute to a more transparent, accountable, and sustainable future.

By embracing the ESRS framework and aligning sustainability with core business objectives, MedTech companies can position themselves as frontrunners in the global shift toward sustainable device development.

Our MedTech experts are ready to help with your pressing questions or challenges related to CSRD and medical devices – simply get in touch to start the conversation.

And stay tuned over the coming weeks for parts two and three of our EU Green Deal Series covering the Corporate Sustainability Due Diligence Directive (CSDD) and the Eco-Design for Sustainable Products Regulation (ESPR).